TL;DR

Hyperliquid is a decentralized perpetuals exchange that built its own L1 blockchain rather than deploying on Ethereum or Solana. The result is 200,000 TPS, 0.07-second block finality, and a fully on-chain order book with zero gas fees on all trades. Its native token, HYPE, was distributed with zero venture capital allocation – every token went directly to users. As of June 2026, Hyperliquid holds approximately 40% of the perpetuals DEX market with $10B+ daily volume and 2M+ active users. It is the fastest decentralized exchange ever built, and also one of the most centralized. Whether that tradeoff works for you depends on what you are trading and how much you need trustless settlement. For active traders prioritizing speed and fee efficiency, nothing on-chain comes close. For institutions requiring credible censorship resistance, the 24-node validator set is a real constraint.

Most people asking what Hyperliquid is already have skin in DeFi somewhere. The short version: it has done to perpetuals trading what Uniswap did to spot – but with a real order book instead of an AMM, and on a blockchain built from scratch to never be slow.

What is Hyperliquid?

Hyperliquid is a decentralized exchange built on a purpose-built L1 blockchain – not a fork of Ethereum, not a Solana program, but a clean-slate chain designed to handle financial transactions at high frequency. It launched mainnet in 2023 and by early 2026 had become the dominant force in decentralized perpetuals trading, handling more daily volume than dYdX, GMX, and Drift combined.

The platform supports perpetual futures on crypto assets (BTC, ETH, and over 150 tokens), spot trading, and as of May 2026, prediction markets via HIP-4. S&P 500 futures with up to 50x leverage went live in early 2026, alongside commodity futures for oil, gold, and silver – a move that signals Hyperliquid is positioning as a general derivatives exchange, not a crypto-only venue. Commodity futures have shown 64% trader retention versus a 27% crypto baseline, which is the kind of number that gets institutional attention.

The key distinction separating Hyperliquid from most DeFi alternatives: every trade settles on-chain with a real order book, not estimated pricing from a liquidity pool. That matters for price discovery, fee efficiency, and manipulation resistance in ways that compound over time and at scale.

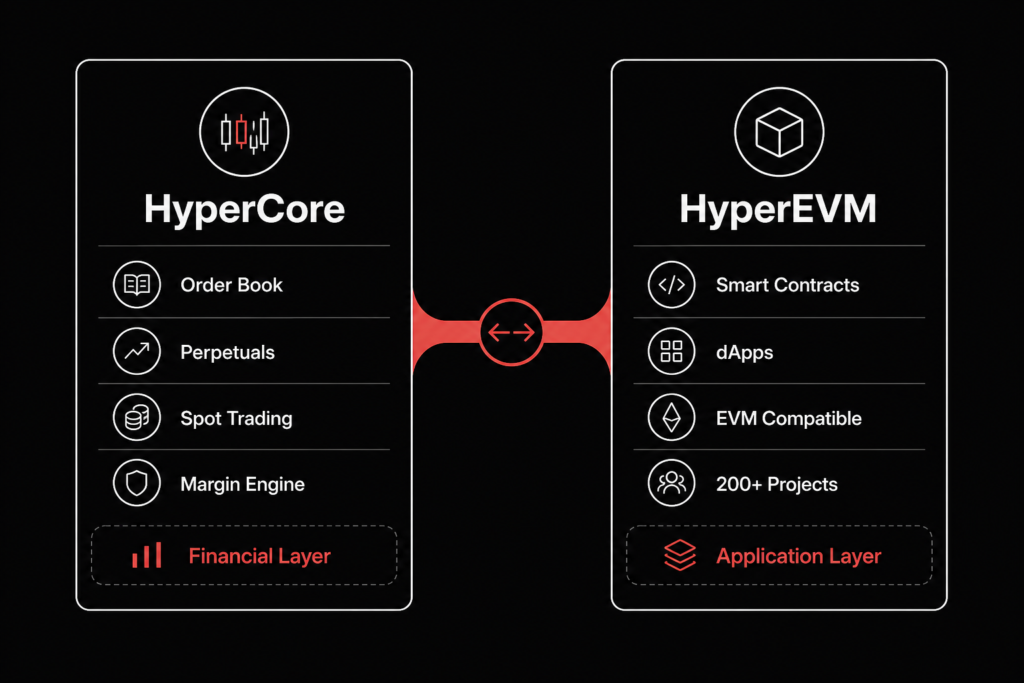

How it works: the two-layer architecture

Hyperliquid splits into two layers running on the same state machine:

HyperCore is the financial primitives layer. It runs the order books, manages margin accounts, handles liquidations, and settles trades. This is where perpetuals and spot trading happen, optimized for throughput: 0.07-second block times with one-block finality, 200,000 TPS capacity, and semantic ordering at the consensus level to prevent front-running. Semantic ordering means orders, cancellations, and liquidations are categorized before matching – no validator can reorder transactions within a category to profit at a trader’s expense. For market makers who have operated on chains where MEV is a constant cost, this architecture is a genuine differentiator.

HyperEVM is the EVM-compatible smart contract layer. Any Ethereum dApp can deploy here with minimal changes. More than 200 projects have deployed on HyperEVM as of June 2026, including DeFi protocols, prediction market apps, and trading infrastructure. The HyperEVM is still in alpha – the team explicitly flags active development and it is not production-hardened for all use cases.

Both layers share the same state machine, meaning a dApp on HyperEVM can read from and interact with HyperCore order books directly – no bridges, no cross-chain latency, no bridging risk.

The consensus mechanism is HyperBFT: a Byzantine fault-tolerant protocol producing one block every 0.07 seconds. Validators that miss proposals are jailed and removed from the active set temporarily. The tradeoff for this performance is a 24-node validator set – the centralization point that generates most of the legitimate criticism of the platform.

Why the order book changes things

Most DEXes use automated market makers: liquidity pools where prices are set algorithmically based on pool ratios. Uniswap, GMX, and Drift Protocol all use variants of this. The advantage is simplicity; the disadvantages are price slippage on larger trades and pricing inefficiency relative to reference markets.

Hyperliquid uses a real price-time priority order book. The best-priced order executes first; among orders at the same price level, the earliest order gets priority. This is how Binance and the NYSE work, and it is what market makers need to operate profitably. The result is tight spreads even at scale – Hyperliquid’s daily volume hit $10B+ in 2026 with execution that professional traders consistently describe as indistinguishable from a centralized exchange.

Reddit and X trading communities consistently cite execution quality as the platform’s primary real advantage, not the decentralization narrative. For a deeper look at how order book mechanics shape your fills, Crypnot’s spot trading guide covers price-time priority from the ground up.

“Speed is real. Honestly feels like trading on Binance minus the KYC nightmare.” – r/defi thread on Hyperliquid, 2026

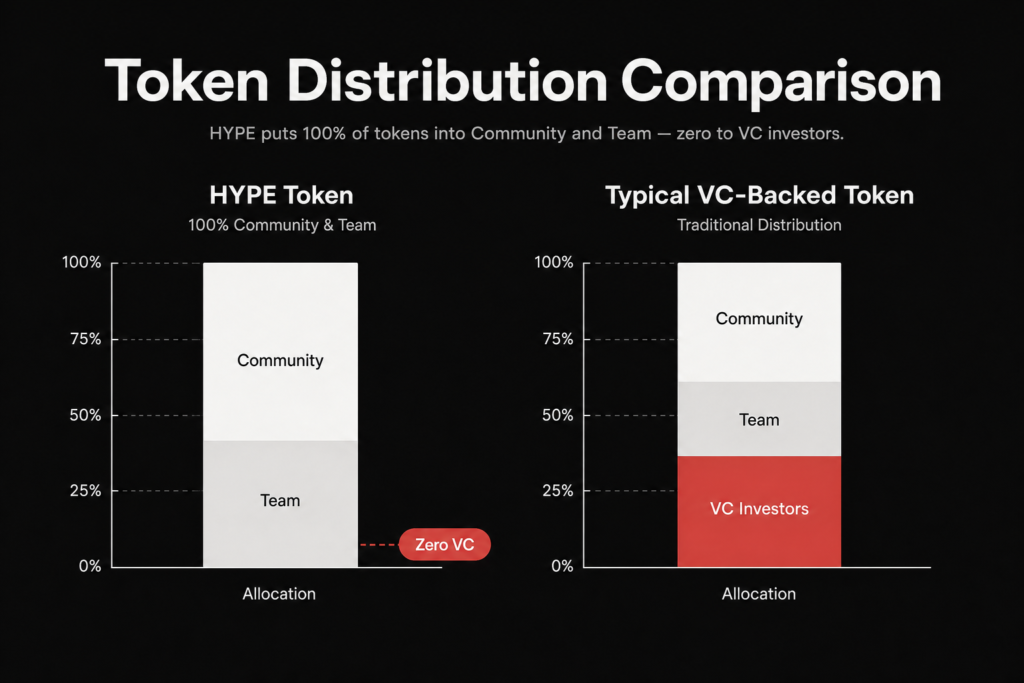

HYPE token: built different

HYPE is Hyperliquid’s native token, and its distribution model attracted more attention at launch than the technology itself. In an industry where 20-30% of token supply typically goes to venture capital before any public access, Hyperliquid allocated zero percent to institutional investors – the entire supply went to core contributors and the community via a Genesis Event.

The reasoning from the team: VC allocation creates governance conflicts (investors want exits, protocols want longevity), pressures for premature monetization, and misaligned incentives between builders and capital. The community took this seriously – the no-VC narrative generates consistently high engagement on X/Twitter and is the primary reason Hyperliquid has a loyal base of retail traders who are not just using the platform but actively rooting for it.

HYPE has three primary uses:

- Governance – HYPE holders vote on protocol parameters, fee tiers, validator conditions, and treasury allocations via the Hyper Foundation governance process.

- Staking – Stake HYPE to earn roughly 2.37% annualized yield at current staking levels (approximately 400M HYPE staked). Stakers also receive fee discounts of 5-40% depending on stake size.

- Buybacks via Assistance Fund – 10% of trading fees are recycled into automated HYPE purchases. As of June 2026, cumulative buybacks total $1.16B. This mechanism – not external capital inflows – drove HYPE to its $62 all-time high in May 2026. Track the live HYPE price on the Crypnot price index.

One supply dynamic worth understanding: HYPE is inflationary through staking rewards and has no fixed supply cap. The community governs the balance between inflation from rewards and deflation from buybacks. Q1 2026 saw $192.25M in buybacks – down from $316.76M in Q3 2025 even as price hit ATH – a declining trajectory that deserves monitoring.

U.S. persons are prohibited from purchasing or holding HYPE under current platform rules.

The HLP vault

The HLP (Hyperliquidity Provider) vault is a community-owned market maker. Users deposit USDC, accept a 4-day lockup, and earn a pro-rata share of the vault’s profits from:

- Market-making spreads (buying the bid, selling the ask across perpetuals markets)

- Funding rate income from perpetual positions

- Liquidation event profits

- 40% of all protocol trading fees

Estimated APY ranges 5-20%, but this is not risk-free yield. If the vault takes directional exposure or gets caught on the wrong side of a large liquidation cascade, depositors absorb the loss proportionally. Before committing, it is worth benchmarking HLP returns against other on-chain yield sources — Crypnot’s breakdown of stablecoin yield sustainability covers the difference between real yield and incentive-driven returns. The vault has generally performed well but has experienced drawdown periods during high-volatility events. The 4-day lockup means you cannot exit quickly if conditions deteriorate.

What it costs to trade

Hyperliquid uses a 7-tier fee structure based on 30-day trading volume. Takers pay; makers earn a rebate at most tiers.

| Tier | 30-day volume | Maker fee | Taker fee |

|---|---|---|---|

| 0 | $0+ | -0.020% (rebate) | 0.035% |

| 1 | $500k+ | -0.015% (rebate) | 0.038% |

| 2 | $5M+ | -0.010% (rebate) | 0.040% |

| 3 | $50M+ | -0.005% (rebate) | 0.042% |

| 4 | $500M+ | 0.000% | 0.045% |

| 5 | $2B+ | 0.010% | 0.050% |

| 6 | $10B+ | 0.020% | 0.055% |

HYPE stakers reduce these rates by 5-40% depending on stake size. Zero gas fees apply to all order placements, modifications, and cancellations on top of this structure – a consistent cost advantage over chains where gas is a meaningful friction point.

At Tier 0, a market maker trading $100M per month earns a rebate on every maker order while paying 0.035% on taker fills. The math is genuinely favorable for high-frequency operations, which is a large part of why institutional market makers have chosen Hyperliquid as their primary on-chain venue.

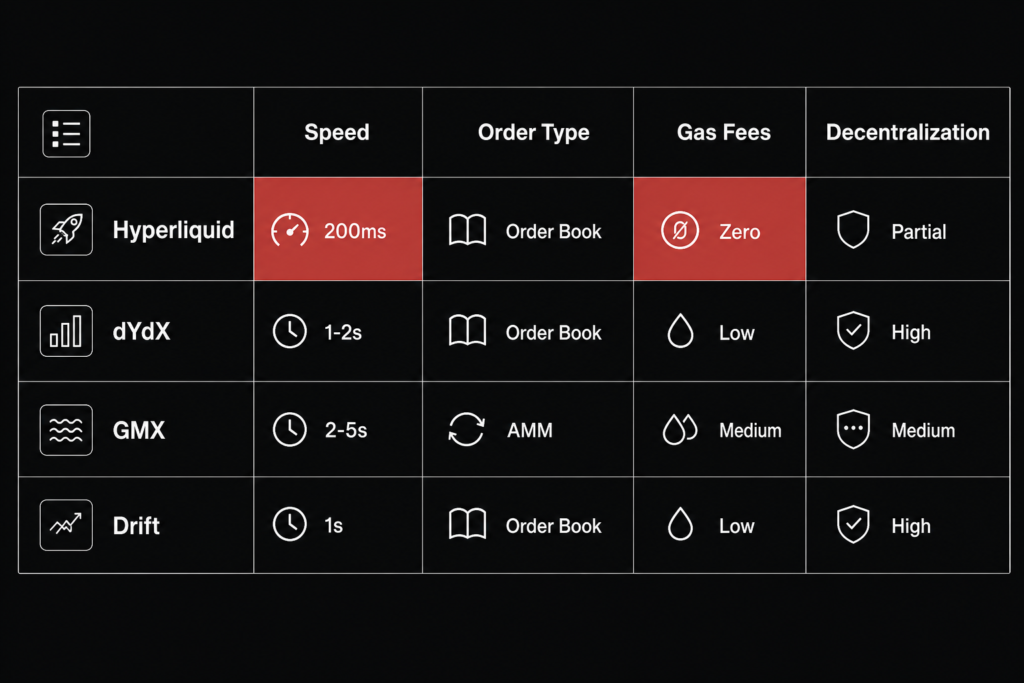

How Hyperliquid stacks up

The perpetuals DEX space has four serious competitors. Here is how they compare on the dimensions that matter most:

Hyperliquid wins on speed and fees. The 200ms median latency is faster than several centralized exchanges for certain order types, and the zero-gas model removes the constant friction that plagues competing on-chain venues. For market makers specifically, negative maker fees mean profitable operations at meaningful scale – a structure that is simply impossible on high-gas chains.

dYdX v4 is the decentralization argument: a larger distributed validator set, longer battle-tested history, and multi-chain architecture at the cost of higher latency and more operational overhead. If credible censorship resistance is the primary requirement – institutional custody, regulatory defensibility, DeFi composability without single-team dependencies – dYdX is the more conservative and defensible choice today.

GMX uses a pool-based AMM structure instead of an order book. For smaller position sizes where slippage is manageable, this works. For market makers or high-frequency strategies, the pool model introduces pricing inefficiencies that Hyperliquid’s order book avoids structurally.

Our read: for active traders prioritizing speed and fee efficiency, Hyperliquid is the clear choice in 2026. For protocols or institutions that need trustless settlement, the current validator count makes dYdX more defensible despite the performance tradeoff. Crypnot’s crypto exchange guide covers fees, security, and features across the major venues – useful if you are still deciding where to route volume.

The risks worth knowing

Centralization is the headline risk that matters. A 24-validator set is fast because it is small – but small validator sets can be coerced, captured, or compelled. The team has publicly committed to expanding the validator set, and a governance transition from the Hyper Foundation to a community-controlled DAO is on the roadmap. Until these materialize, Hyperliquid should be treated as a high-performance trading venue with centralized trust assumptions, not a censorship-resistant settlement layer.

Platform maturity is the second risk. Ghost fills – orders appearing executed but not settling – have been reported. The JELLYJELLY incident and occasional market breaks during extreme volatility indicate an early-stage platform that has not yet weathered a full crypto bear market cycle. The team responds quickly to issues. The track record is short.

HYPE token dynamics warrant attention separately from the trading platform. The $1.16B in automated buybacks has structurally supported HYPE price, but quarterly buyback volume declined from $316.76M (Q3 2025) to $192.25M (Q1 2026) even as the token hit ATH – a divergence between price performance and underlying buyback support that is worth tracking.

What has changed in 2025-2026

The platform’s scope has expanded substantially. HIP-4 prediction markets launched in May 2026 with 6.05M BTC contracts traded in the first 24 hours – meaningful early traction that fits a broader trend of new entrants pushing into crypto perpetuals territory. S&P 500 futures with up to 50x leverage and commodity futures (oil, gold, silver) went live in early 2026, pushing Hyperliquid further toward general derivatives exchange territory.

Bitwise described Hyperliquid as the “1,000 pound gorilla” of the perpetuals DEX space – apt for a platform holding 40% market share while HYPE returned +54.8% YTD during a period when the broader crypto market shed $564.3B.

The HyperEVM ecosystem has reached 200+ deployed projects, with community-led development happening without Foundation funding. The validator expansion roadmap and governance decentralization plan remain the two variables with the most asymmetric impact on long-term trust in the platform.

Frequently Asked Questions

- What is Hyperliquid?

Hyperliquid is a decentralized perpetuals exchange built on its own L1 blockchain. It uses a fully on-chain order book (HyperCore) alongside a smart contract layer (HyperEVM), achieving 200,000 TPS, 0.07-second block times, and zero gas fees on all trading activity. - Is Hyperliquid truly decentralized?

Partially. Trading infrastructure runs on-chain with transparent order books, but the validator set is currently only 24 nodes. That makes full censorship resistance unrealistic today. The team has committed to expanding the validator set, but the centralization tradeoff is real and worth understanding before committing significant capital. - What is the HYPE token?

HYPE is Hyperliquid’s native governance and staking token. Its defining feature is zero VC allocation – all tokens were distributed directly to users via the Genesis Event, with no institutional investor allocations. HYPE earns roughly 2.37% annual staking yield and grants fee discounts of 5 to 40% on the platform. - How do Hyperliquid trading fees compare to Binance?

Hyperliquid charges zero gas fees on all trades. Taker fees start at 0.035% and maker fees are negative – you earn a rebate – at most volume tiers. Compared to Binance’s standard 0.1% taker fee, high-frequency and market-making strategies can be significantly cheaper on Hyperliquid, especially at higher 30-day volume tiers. - What is the HLP vault and how do I earn from it?

The HLP (Hyperliquidity Provider) vault is a community-owned market maker on Hyperliquid. Users deposit USDC, lock it for 4 days, and earn a pro-rata share of market-making profits, including spreads, funding rates, and 40% of all protocol trading fees. Estimated APY ranges from 5 to 20%, though it fluctuates with market conditions and drawdown risk exists.

Disclaimer

This content is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. Cryptocurrency markets are volatile. Always do your own research and consult a qualified professional before making financial decisions.