TL;DR

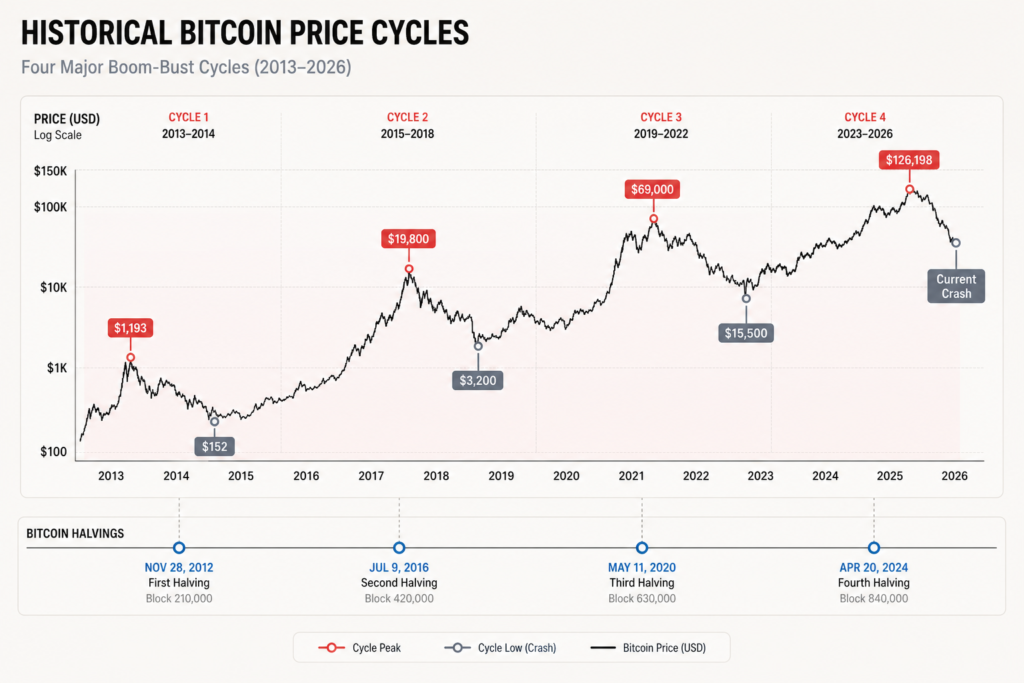

Bitcoin is at an inflection point. The October 2025 peak of $126,198 followed the historical pattern of topping ~1.5 years after the April 2024 halving, but the subsequent 52% correction to $60,074 has reopened a fundamental debate: Is the traditional four-year cycle dead, or reasserting itself?

The bull case rests on structural changes-institutional adoption via $87 billion in ETF inflows since January 2024, regulatory clarity, and a suboptimal 0.5% penetration of US advised wealth creating a massive growth runway. The bear case cites historical precedent: Prior cycles saw 77-90% declines, and hashrate staying at all-time highs while price falls could signal incomplete capitulation.

Most institutional analysts lean bullish for 2026, with targets ranging from $100K to $150K+-but the range of expert forecasts spans $40,000 to $225,000, reflecting real uncertainty about whether this cycle breaks the pattern.

The Debate

Bitcoin in June 2026 is facing its most consequential question since institutional capital arrived: Does the traditional boom-bust cycle still govern digital assets, or have structural changes fundamentally altered the rules?

The debate isn’t academic. It determines whether current lows near $60,000 represent capitulation into a multi-year bear market or a dip within a longer institutional adoption cycle. It shapes allocation decisions for family offices, sovereign wealth funds, and corporate treasuries. And it separates the bears who forecast $40-65K lows from the bulls targeting $150,000+ before year-end.

To understand where this goes, you need to understand what changed-and what didn’t.

The Bull Case

The institutional structure is real. Bitcoin is no longer a retail novelty. The SEC’s approval of spot Bitcoin ETFs in January 2024 was the inflection point. In the 18 months since, global crypto ETPs have attracted $87 billion in net inflows, with US Bitcoin ETPs alone holding ~$97 billion in assets. These aren’t speculative retail flows-they’re allocation decisions from Harvard Management Company, sovereign wealth funds, and wealth management platforms completing their due diligence on crypto as an asset class.

What matters: It’s steady. Prior bull markets were feast-or-famine. The ETF flows aren’t working like that. They’ve been consistent quarter-over-quarter, suggesting this isn’t a bubble-it’s capital allocation finding an asset class it previously couldn’t access.

Penetration is still early. Less than 0.5% of US advised wealth is in crypto. With US advised wealth totaling roughly $40 trillion, that $220 billion in crypto represents a rounding error. Even a rational 5% allocation to digital assets would represent a 50-100x increase in capital. Standard allocations now include alternatives-commodities, hedge funds, REITs-in 5-10% slices. BTC -0.20% and ETH +0.10% are beginning to occupy that bucket.

This runway isn’t priced in because it hasn’t happened yet. See our market outlook and penetration analysis for the detailed math.

Supply is fixed and verifiable. Bitcoin’s supply is capped at 21 million coins, hardcoded into the protocol. The 20 millionth Bitcoin will be mined by mid-2026. By contrast, fiat currency supplies are expanding continuously-the US debt-to-GDP ratio is at historic highs, the dollar faces debasement risk, and central banks have no binding constraint on printing. Bitcoin’s scarcity is algorithmic and verifiable. For institutions facing currency debasement, this is a legitimate store-of-value narrative.

The four-year cycle is structurally broken. Historically, Bitcoin peaked roughly 1-1.5 years after each halving, then entered a bear market lasting until the next cycle. The pattern held for cycles in 2013, 2017, 2021, and appeared to repeat with the October 2025 peak. But institutional analysts argue that institutional capital flows are replacing retail-driven cycles. Retail bubbles are volatile and binary. Institutional capital is methodical. It compounds. It doesn’t evaporate.

If this is true, the 52% correction is a healthy pullback, not a bear market signal. It’s noise in a longer uptrend.

Regulatory clarity is a genuine tailwind. The SEC’s approval of spot Bitcoin ETFs, the 2025 GENIUS Act providing stablecoin regulation, and expected 2026 bipartisan crypto market structure legislation reduce existential risk for Bitcoin. Institutions don’t allocate to existential risk-they allocate to regulated assets with clear rules. Each regulatory milestone unlocks another tier of capital.

Expert consensus leans bullish. Major institutions expect Bitcoin to reach new all-time highs in H1 2026, with targets ranging from $100K to $150K+. These aren’t retail cheerleaders-they’re institutions with reputation at stake. See our institutional forecasts and long-term investment analysis.

The bull case is: The structure has changed, penetration is early, supply is fixed, the regulatory path is clearing, and institutions moving capital now are smarter and more patient than the retail crowds that drove previous cycles.

The Bear Case

The historical pattern is ironclad. Bitcoin’s four-year cycle is one of the most reliable patterns in financial assets. Previous bear markets saw 77-90% declines from peak to trough. The 2013 cycle peaked at $1,193 and crashed to $152. The 2017 cycle peaked at $19,800 and fell to $3,200. The 2021 cycle peaked at $69,000 and bottomed at $15,500.

The October 2025 peak at $126,198 timed perfectly with historical precedent-approximately 1.5 years after the April 2024 halving. If the pattern holds, Bitcoin is now headed for $40-65,000 lows, possibly extending through 2026. The 52% decline so far is well within historical ranges and suggests capitulation is incomplete.

Macro headwinds are real. The bull case assumes continued Fed support and deflation-driven demand for alternative assets. But the macro environment is fragile. The Fed cut rates three times in 2025 and may cut further in 2026, but this could reverse quickly if inflation resurfaces or growth falters. A recession scenario or stock market correction typically triggers “risk-off” selling, where Bitcoin crashes alongside equities as investors flee to cash and bonds. If the economy slows and the dollar strengthens, Bitcoin could face headwinds it hasn’t seen since 2022.

Hashrate disconnect is a warning signal. Bitcoin’s hashrate hit all-time highs around 1,065.7 EH/s in November 2025, yet price has fallen 52%. This is unusual. Hashrate staying elevated while price falls can signal that capitulation is incomplete-miners are mining at losses now but will eventually shut down, potentially triggering further price weakness. Historically, when miners give up, price falls accelerate.

Institutional allocation may already be priced in. This small penetration might already reflect rational institution behavior. Institutions may have done the math and concluded that a small allocation makes sense-not because it will 50-100x, but because 2-3% diversification is prudent. If the current $97 billion in Bitcoin ETFs represents rational institutional demand, then future inflows may not be as explosive as bulls project. The easy capital may already be in.

Technical analysis points lower. Elliott Wave International forecasts Bitcoin to decline further, viewing the October 2025 peak as a completed bull market top. See our technical analysis and breakout patterns for detailed charts.

Retail adoption is declining. Global retail crypto activity fell 11% year-over-year in Q1 2026. Bitcoin’s transaction volume reflects mostly financial positioning (traders), not adoption for payments or utility. This weakens the “fundamental growth” narrative and leaves Bitcoin vulnerable to positioning unwinds.

The bear case is: The cycle has proven remarkably consistent, current weakness is only halfway through historical bear markets, macro conditions are fragile, and institutional capital may be less transformative than bulls assume.

The Key Debates

1. Is the four-year cycle actually dead?

This is the central disagreement. Institutional analysts argue that structural changes-ETPs, regulatory clarity, corporate adoption-have broken the historical pattern. Steady institutional flows replacing retail bubbles means less volatility, steadier uptrends, and an end to the boom-bust cycle.

Traditionalists counter that the October 2025 peak timing matches the historical pattern perfectly, and that claims of “this time is different” have preceded every previous bear market. A 52% decline from peak is actually one of the shallowest in history-which cuts both ways. It could mean the cycle is breaking (bullish), or it could mean capitulation is incomplete and deeper lows lie ahead (bearish).

2. How much institutional capital is actually coming?

The <0.5% penetration estimate implies a massive growth runway. But this assumes institutions will allocate 5-10% to crypto-a bold assumption. Institutions might rationally conclude that 1-2% is appropriate, which means the runway is 2-4x, not 50-100x. This changes the price target dramatically.

3. Are regulatory wins priced in?

The bull case assumes regulatory clarity is still to come. The bear case counters that the SEC approved spot ETFs in January 2024, the GENIUS Act passed in 2025, and crypto is now in the regulatory infrastructure. These wins may already be reflected in valuation. Further regulatory wins might move the needle less than bulls assume.

4. Is store-of-value demand sustainable?

Bitcoin’s bull thesis increasingly rests on its role as digital gold-a store of value against currency debasement. But this relies on persistent inflation or currency weakness. If deflation takes hold instead, Bitcoin’s value proposition weakens. Gold’s value proposition has proven durable for thousands of years. Bitcoin’s track record is 17 years. The jury is still out.

For Institutions

If you’re managing a large pool of capital, here’s what this uncertainty means in practice:

1. The allocation case is sound. Less than 0.5% of advised wealth in crypto, versus 5-10% in alternatives broadly, suggests under-allocation by historical standards. Even a modest 2-3% allocation is rational diversification-not a bet on explosive growth, but a hedge against fiat currency risk and a non-correlated asset.

2. Timing is speculative; conviction is durable. Whether Bitcoin bottoms at $40,000 or $60,000 is a timing question. The structural case-institutional adoption, regulatory clarity, supply scarcity-is a conviction question. If you believe in the conviction, entry points matter less than dollar-cost averaging over 12-24 months.

3. ETPs have changed the game. Spot Bitcoin ETFs have removed custody and operational complexity that kept most institutions out. The $97 billion in US Bitcoin ETPs prove this. You can gain exposure without operating a digital asset team. This reduces friction and accelerates adoption.

4. Corporate treasuries are a new buyer. MicroStrategy, Tesla, and other corporates are accumulating Bitcoin. If this trend accelerates, it’s a structural source of demand you need to account for. See our corporate treasury analysis for real-time holdings.

5. Hashrate strength suggests long-term viability. Miners investing at all-time hashrate despite the 52% price decline is a credible signal of conviction. It doesn’t guarantee price recovery, but it does suggest the network isn’t on the verge of collapse. For institutions, this reduces existential risk.

6. Scenario-plan your allocation. Run three scenarios: bear case ($40K lows, 2-3 year recovery), base case ($100-130K by end-2026), and bull case ($150K+). Size your allocation so you’re comfortable in the bear case, positioned for the base case, and optionally upside-leveraged for the bull case. Our investment scenario guide walks through this framework.